Month 9 Update: Beach House Fund – How To Start Investing And Make Your First $100K!

May 2024 Update

Introduction

Welcome to the Monthly Update of the Blind Luck Beach House Project!! Where I walk you thru starting with ZERO to making your first $100K

They say making your first $100K is the hardest and once you’ve done it you’re 1/3 the way to a million because the compounding effect of just getting started is huge!!

For a detailed write up on why the first $100K is so important plus a some handy calculator tools showing you how long it will take check out this months post How Long Will It Take To Make Your First $100K?

My Goals

It’s always good to be specific when you set out on a new project or journey so you know what success looks like, so let’s refresh ourselves on what my goals are here. I outlined this process in my S.M.A.R.T. Goals What They Are & How To Use Them post. You can also find a good example of goal setting in my 2024 New Years Goals update where I write down and break down the details for my top 5 goals for 2024. (Which include this The Beach House Fund of course!)

So lets revisit the Beach House goal

Goal - High Level

Buy a beach house or have enough invested so I can rent a beach house whenever I want anywhere I want without thinking about money.

Specific Goals (The How):

Have $100,000 Invested

Within 5 years (by end of 2028)

Monthly Updates for accountability

Show others how to start from $0 and become financially independent

What I want to do is encourage anyone who has $0 to get started, and make a life changing amount of money

In 2024 the main focus is going to be to save $10,000 by the end of the year.

Now you might be scratching your head. $100,000/ 5 years is $20,000/ per year. Why isn’t that my number? well 2 reasons

Well that’s actually a good question.

The math says I should have by the end of 2024 $15,984.50 or roughly $1,384.48 / month moving forward. (This assumes a consistent 8% return.

I did this math in my Milestone #1 Check-In Post you should check it out I have a nifty monthly contribution web calculator you can use for your own planning purposes.

I’m going to update my 2024 with a stretch goal that matches what the math says I should have saved by the end of 2024. Now since I’m not sure if I can hit the full amount I’m going to add it as a “stretch goal” so I can keep it in focus but acknowledge it’s going to be a challenge for me this year to hit.

Updated 2024 Goals:

Goal: $10,000 by end of 2024

Stretch Goal: $15,984.50 end of 2024

Progress Update

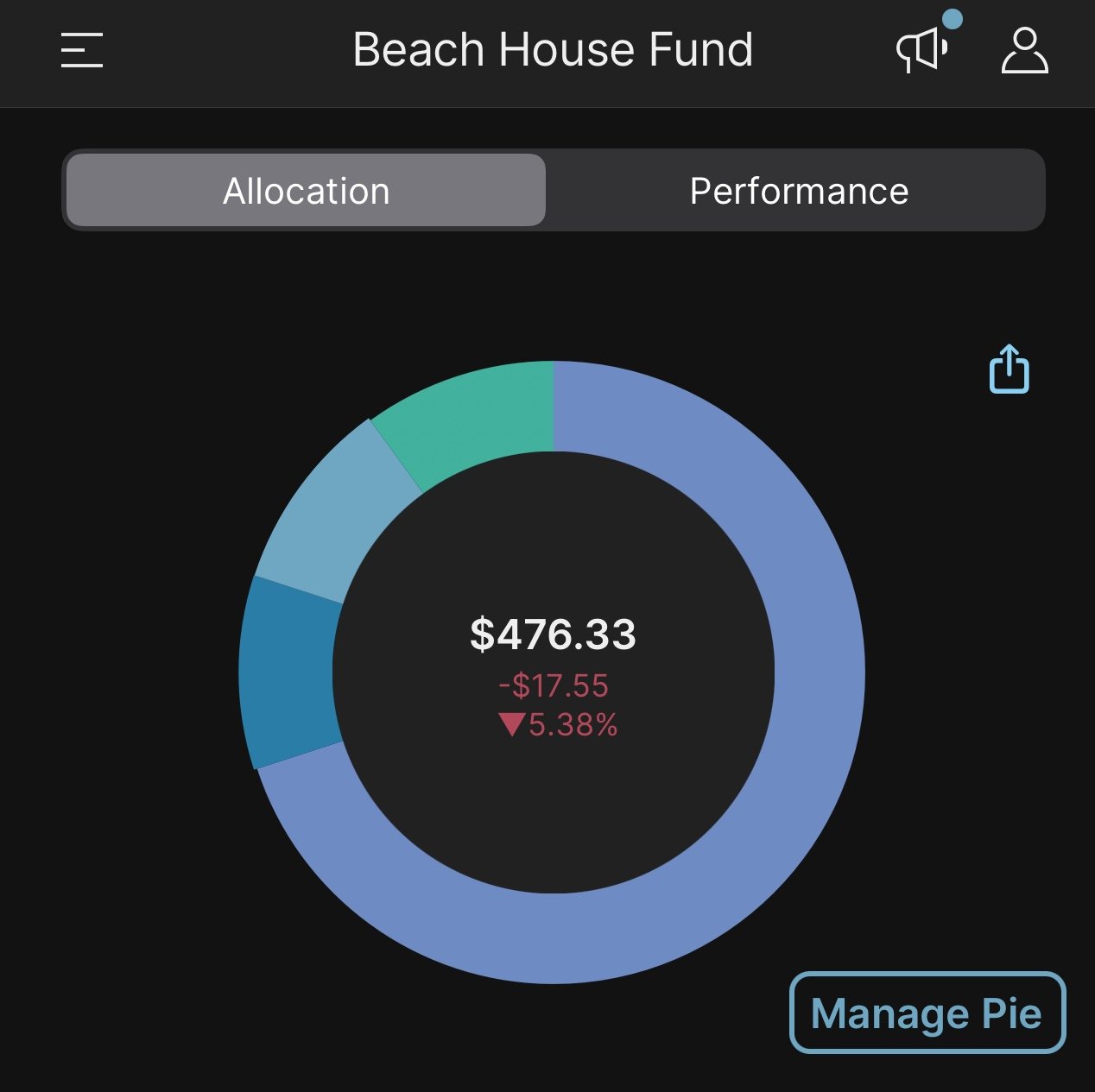

In May 2024 I made the following contribution. .

May2024 Contributions:

$100 Regular Income

$93.31 CC Cash Back

$105.02 X Ads Revenue

$1,000 New Card Signup Bonus (Free $$ why not!)

$1,298.33 Total

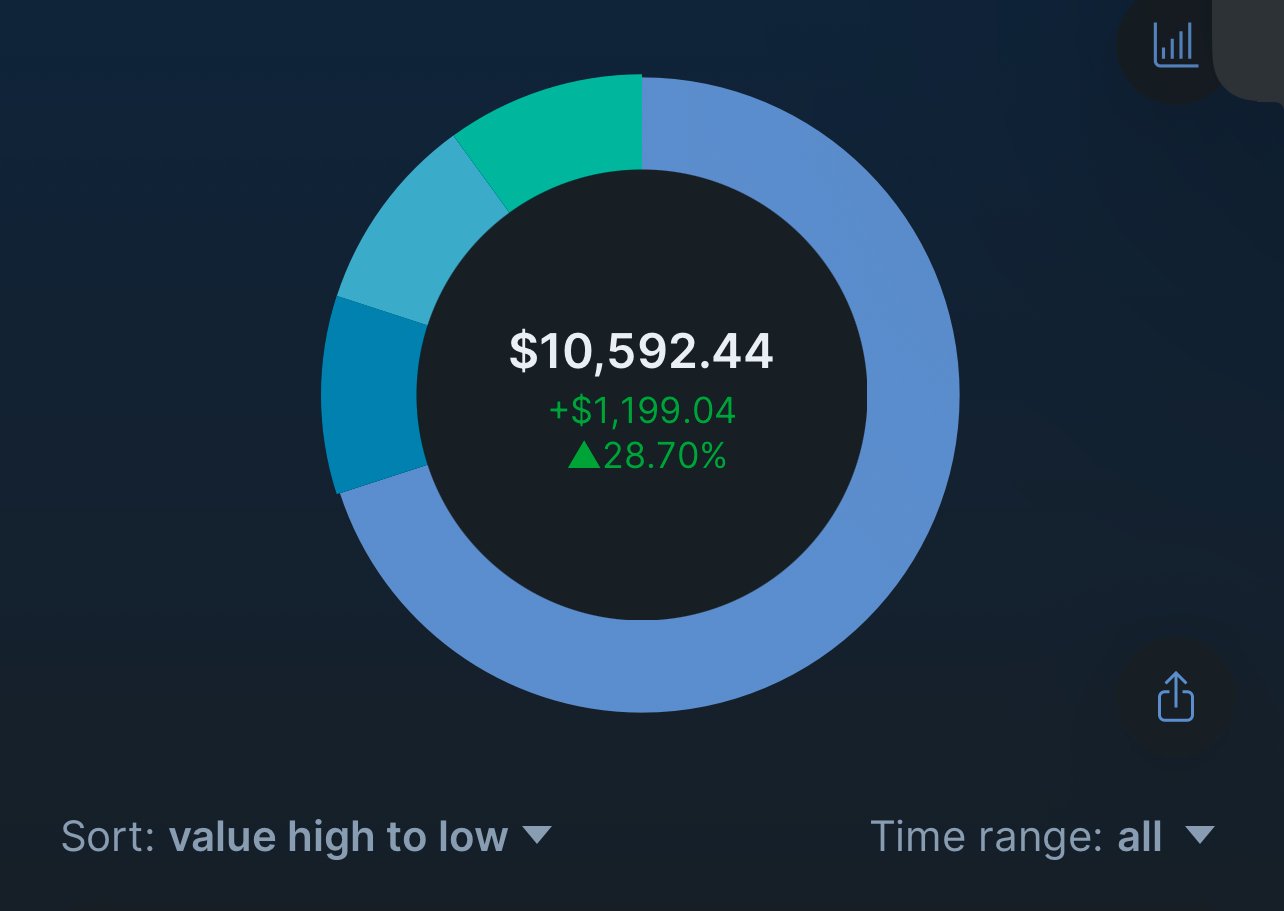

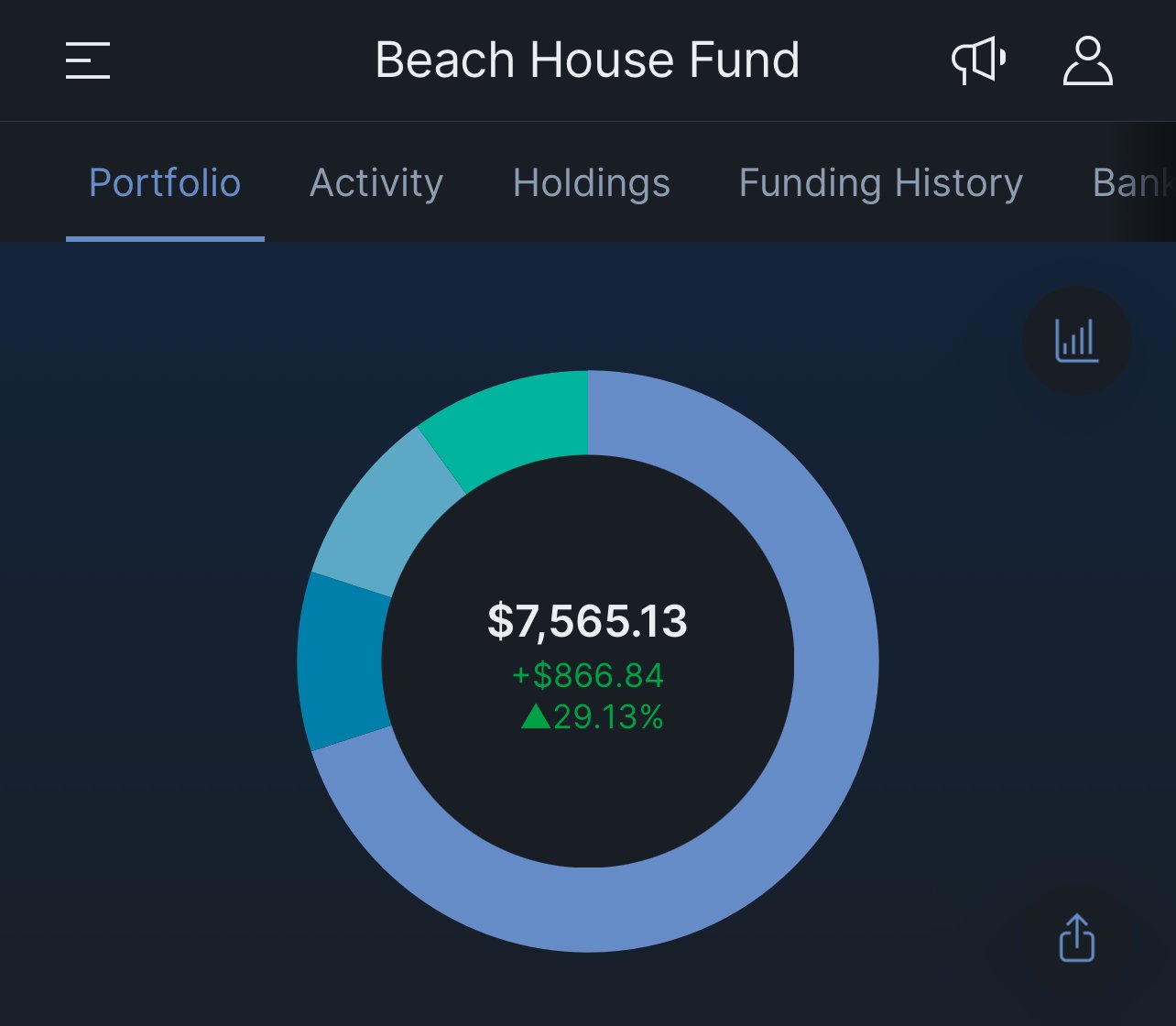

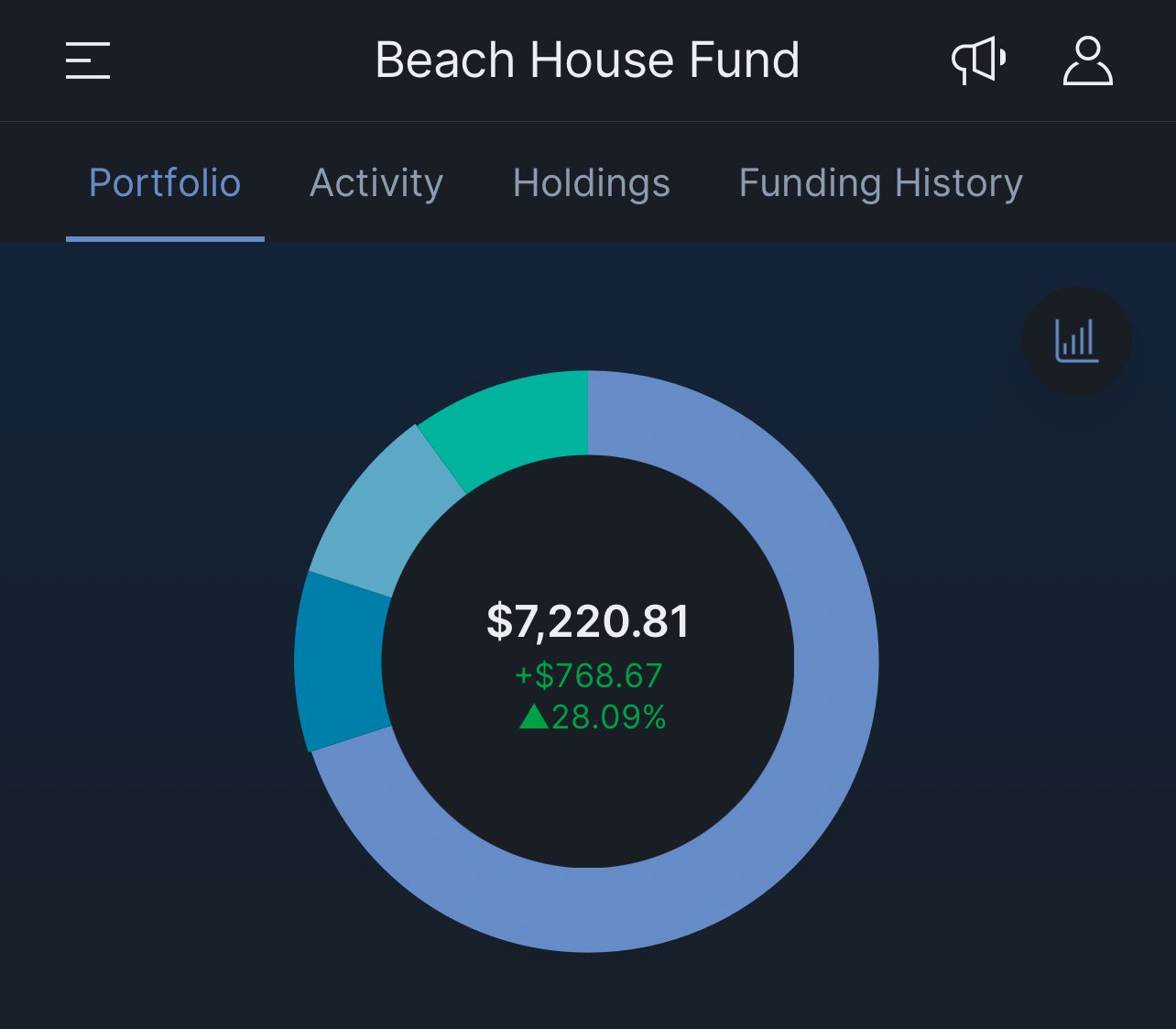

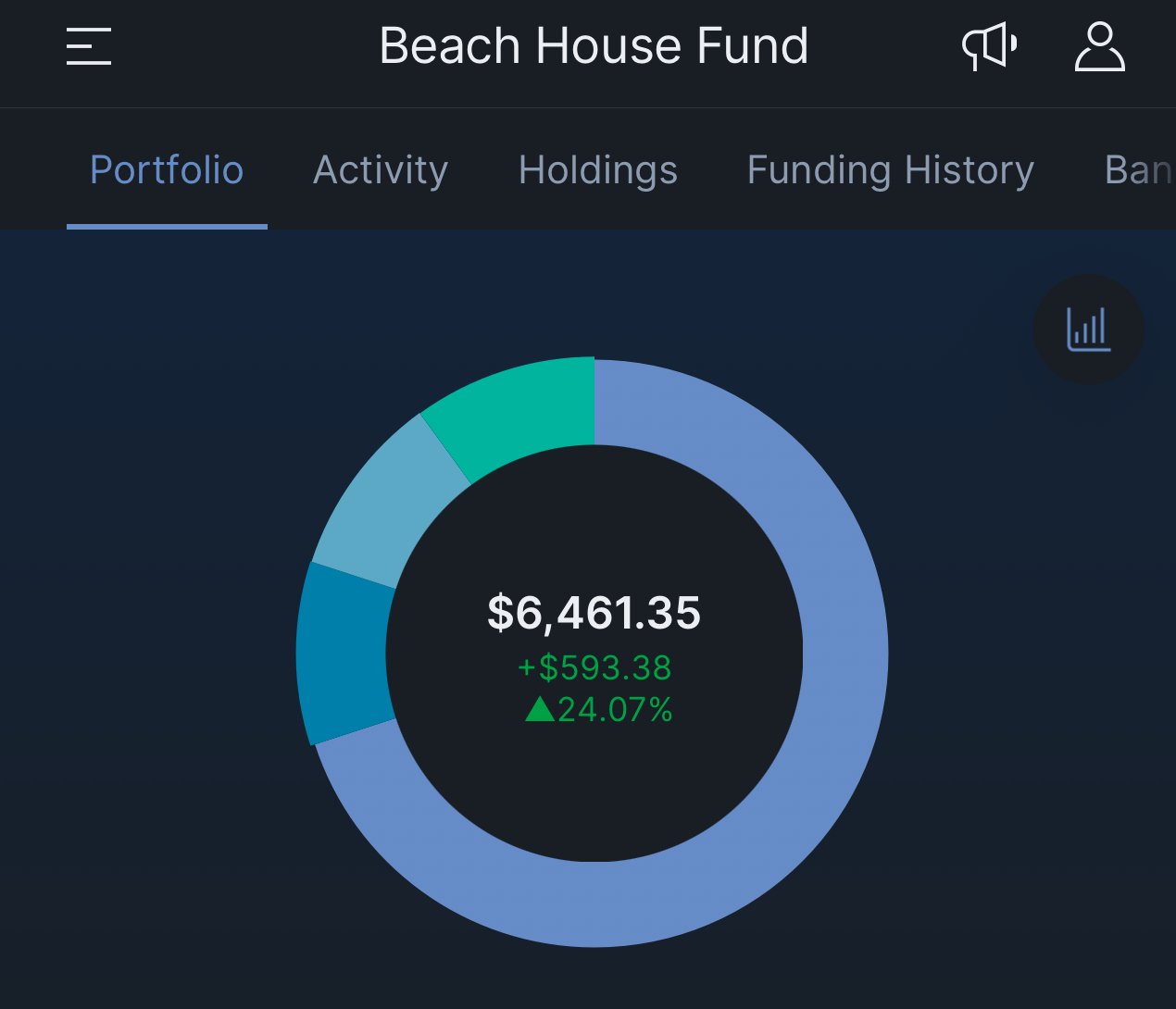

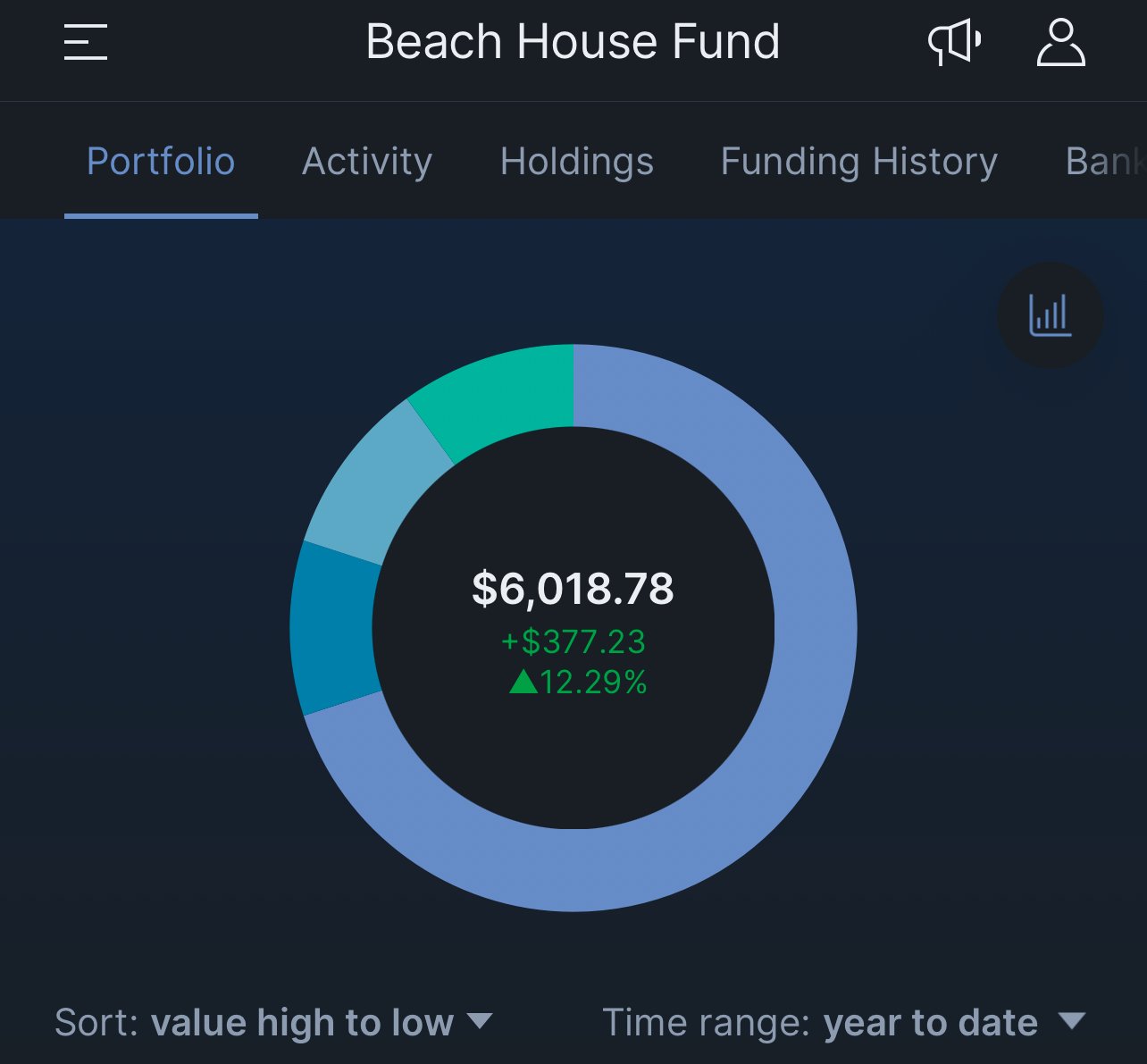

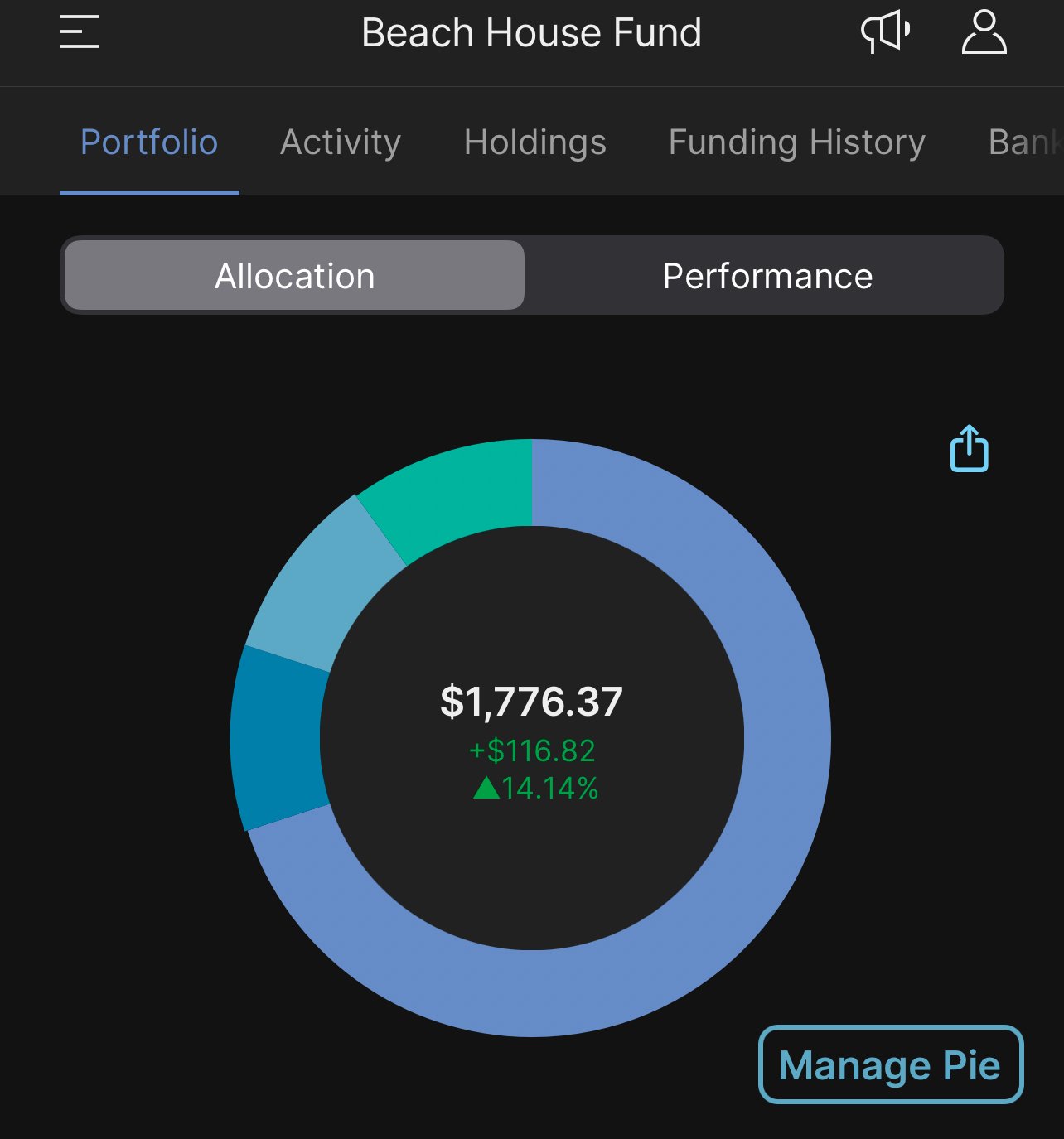

Fund Total: $5,653.42

Slowly but surely we are getting there!

Total progress to date!

The Details

Over all the first 9 months of the Beach House Fund Have been fantastic! We are making meaningful progress toward our goal.

Let’s review the numbers so far.

$5326.30 Total Cash Contributions

$327.05 Market Gains

$25.25 Total Dividends Received

Portfolio Total $5,653.35

Something I want to pint out here is this is month 9 of this fund. my returns on this portfolio have been 20.06% since I started. Which is pretty damn good. That being said. only $352.28 or 6.23% of my portfolio total, this is because some of these returns were when my account was much smaller. as it gets bigger the returns will reprint a larger portion of my growth when compared to my monthly contributions. for example this month alone I contributed almost 3X as much cash as my portfolio has returned since it was started. we are doing. hard carry until the account is bigger.

You are better off in this phase to play it safe and focus Ono your contributions than trying to get market beating returns. it’s not going to matter too much until you get well over $10K saved up. you’re better off keeping your risk profile low and growing the account thru your contributions.

Not much more to report this month, just like hiking, step by step we are making progress.

What I’m invested in

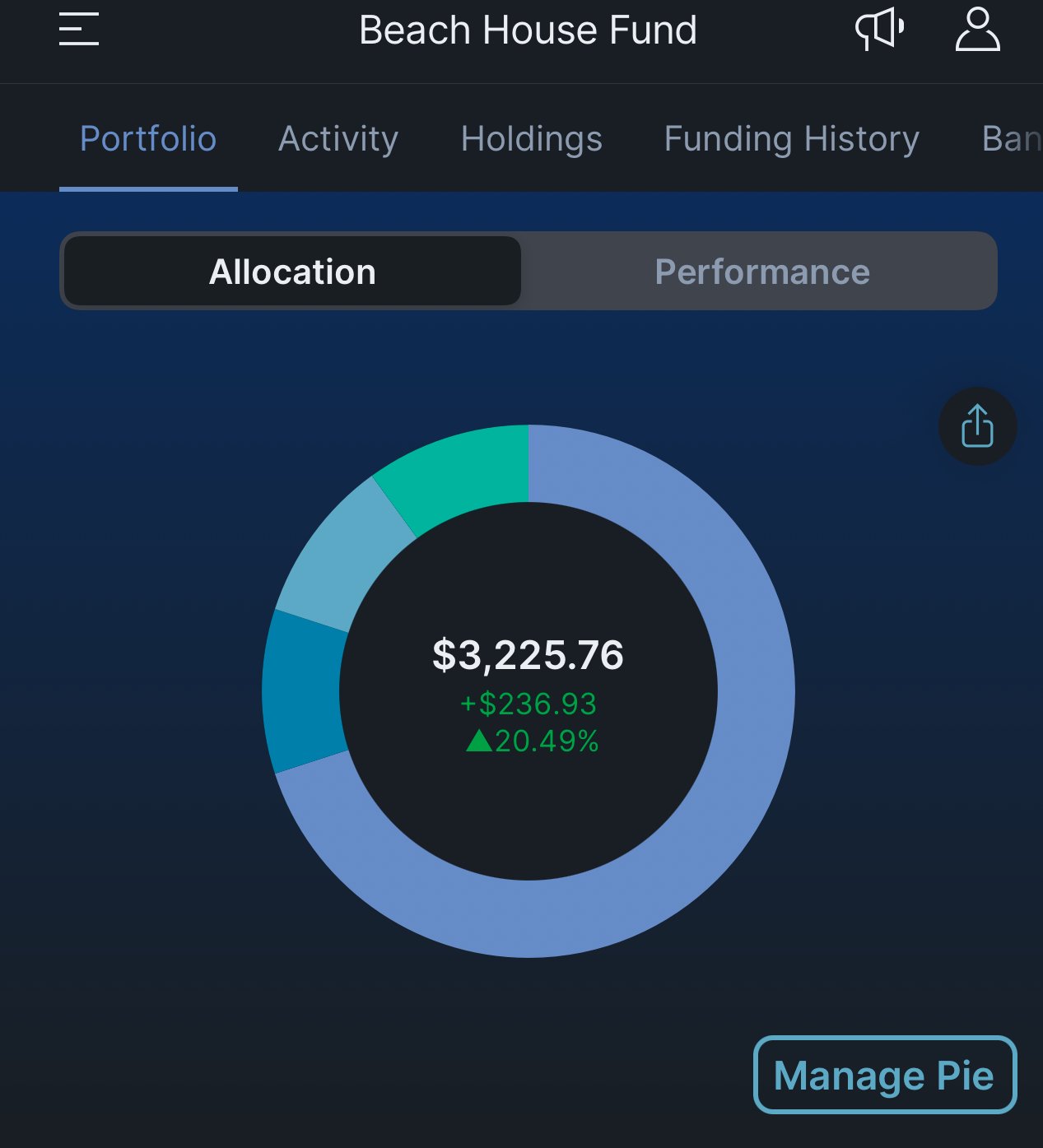

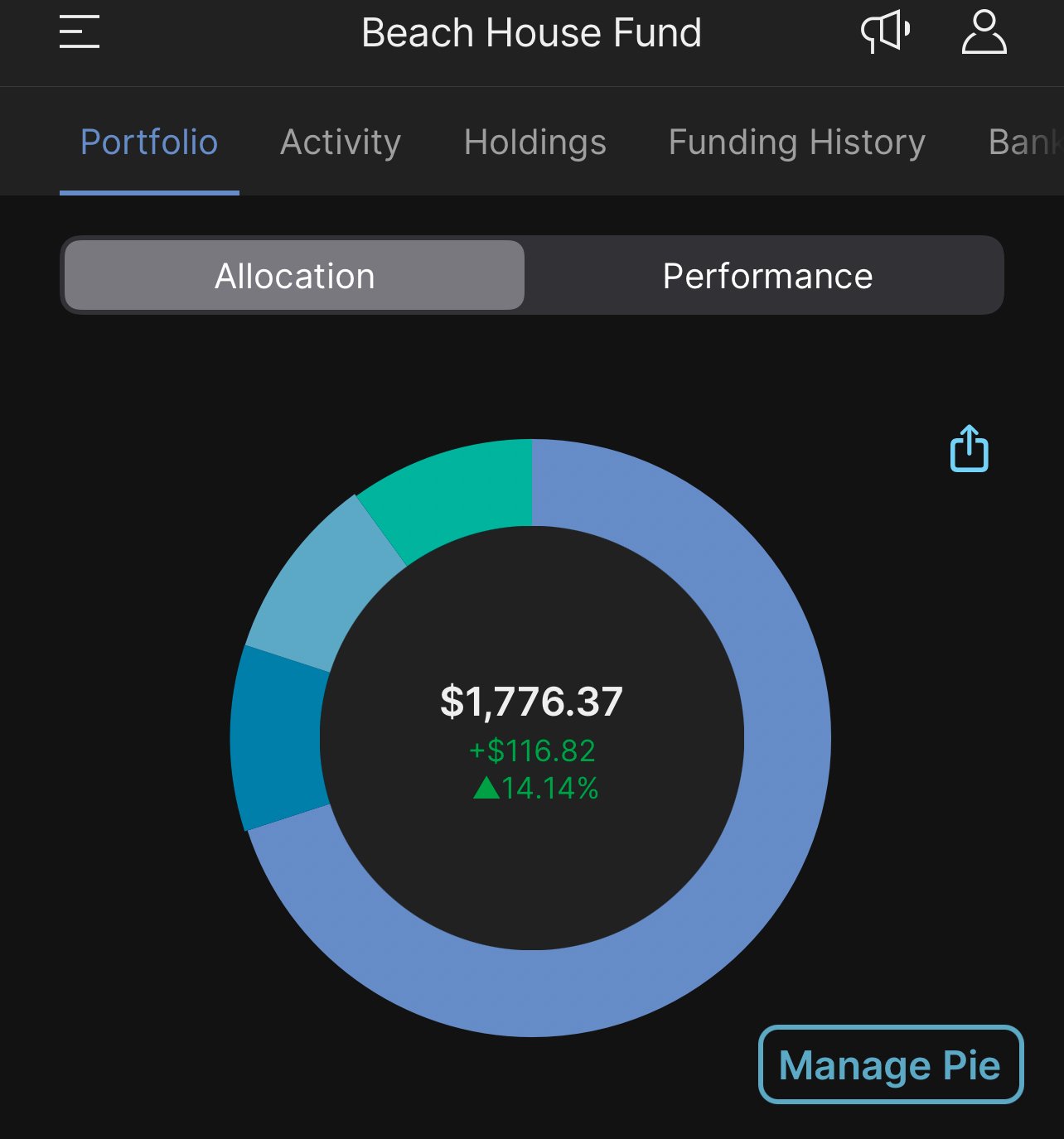

Investment Allocations

In my original post for this project I outline the strategy behind my allocations, you can use whatever you’re comfortable with. Personally I feel safest with a well diversified index portfolio. I talk about what risks I’m trying to manage in My Simple 3 Fund Strategy article. Do your own research everyone’s life situation and finances are different. I’m a slow and steady kind of guy when it comes to investing but I also have healthy emergency fund reserves so I can tolerate some volatility.

As a quick reminder here are my target allocations.

70% $VOO SP500 Fund (S&P500 fund)

10% $SPHD (SP500 High Dividend Fund)

10% $JEPI (JPMorgan Equity Premium

10% $VXUS Total International Fund

M1 Finance Introduced a $3/ Month “Platform Fee”

I do want to address the new $3/ month “Platform Fee” that M1 Finance has introduced for all users with balances under $10K (this includes me!)

May was the first month that this fee was charged (mine came thru on May 15th)

M1 Finance has announced they will start charging a $3/ month platform fee for users with account balances less than $10,000 and don’t already pay for M1+ pic.twitter.com/JWfgaM1koU

— Blind Luck Project (@Blind__Luck) March 15, 2024

While I don’t agree with the move, and I know I’m not alone in this as there has been a lot of venting on social media regarding this change, I don’t plan to move my account.

Here’s why:

This account will be over the $10K minimum within the next 12 months (less than $36 in fees total)

They have added their “M1+ “ features for all users so there is some perceived value, such as better margin loan rates, analytics etc. While I don’t have any immediate plans to utilize these features it’s nice to have them should I choose to use them.

Other platforms such as Robin Hood have a $5/ month for these same features. So M1 is actually cheaper

A plan consistently executed is better than a new plan every few months. While this fee isn’t ideal I feel my energy is best focused on continuing to invest, regardless of the platform.

The main reason I don’t agree with the M1 Finance change is how they announced it. I feel it should have been an opt in feature for existing users and they could have implemented the fee for new users. It feels underhanded when people sign up expecting a “Free” simple to use brokerage only to find out later that they want to start charging a fee.

Overall I understand why they are making this change, lots of small accounts tend to add extra overhead to a company who has to do compliance reporting, and provide customer support for every customer, even if they have very small accounts.

That being said many small accounts are going to be younger individuals and other brokerages such as Robin Hood are offering the ability to opt in. I think this is a better approach as they can capture and retain users earlier in their investing journey and benefit as their accounts grow with their future earning and investing power.

All this being said, M1 still meets my needs for this goal of saving for a beach house and I have no plans of moving my account.

For more uptodate news on issues such at the new M1 Finance Platform Fee and how they might affect you, make sure to follow me over on X @Blind__Luck