How Much Do I Live on As A Retired 34 Year Old?

Pretty colors to show how much cash I hemorrhage every month

Table of Contents:

Introduction

My Monthly Expenses

Summary/ charts

Numbers don’t add up

Future Savings

What about Emergencies?

Closing Thoughts

Introduction

While I don’t keep a budget I do check in on my spending every couple months to make sure I’m not overspending. With inflation on the rise and the markets looking a little Shakey I thought the end of the 1stquarter offered a good opportunity to review my spending and share with you guys how much it costs me to live a retired life style.

As we go thru this I’m not going to tally things up to the last penny, because well that feels too much like work :P. I’ll be sharing round numbers that are easy to digest. Just for a little background that I shared in my How I Retired At Age 32 Post I make around $66K passively every year thru non investment income. My goal is to save around $20K of that and reinvest any investment income I may have. I also have a side hustle that pays me around $500-1,000 / month that helps me hit that $20K number. For the purposes of this analysis we’ll assume I have income of $66K per year or around $5,500/ month.

On a final note before we get into the numbers keep in mind I’m already retired so I may not be pinching every penny like some of you working toward the goal of FIRE. Also I plan to let my lifestyle grow over the years as my investment “safety net” grows, but for now my best tool is to keep my costs low and let time work for me. Some of my expenses such as housing will eventually go to zero as I get older freeing up additional monthly savings.

So here we go!

My Monthly Expenses

Housing $1,602 (29.1%)

Mortgage 1,203 / Month

HOA $113 / Month

Insurance/ Taxes $286 / Month

Having your living expenses locked in when your retired is very important. Regardless of what the real-estate market does you want to be able to keep this costs fixed and predictable. I bought a 3 bedroom 3 bath 1,925 SF house in 2020 for $333K right after I retired. I plan to do a fair amount of travel over the years and maybe even rent a place out for periods of time. But retiring at such a. young age I knew I needed to insulate myself from the ever growing costs of rent. While 29.1% of my income seems like a lot, this number will shrink as my passive income continues to grow, and eventually I’ll own this home free and clear.

Health InsuΩrance $750 (13.6%)

Yep you read that right! $750 for one person! People in the FIRE community talk about this and it’s a real thing, especially if you have a family medical insurance can be a major drag when you have to pay out of pocket. My current polic is the COBRA policy from my former employer, it’s very good insurance but it’s EXPENSIVE over half my mortgage! Ouch! Good thing is I’m coming off this plan this year and will be finding a more affordable option. Shouldn’t be hard to improve this number in the future!

Utilities: $660 (12.0%)

Gas $35

Water/ Sewer/ garbage $95

Electricity $150

Bug Guy $40

Landscaping $50

Phone $65

Internet $60

Cleaning Lady $165

(These numbers have been averaged over the past 12 months)

This is a category I could cut back on if I ever needed to save some money. Do I need a cleaning lady, Landscaper, or guy to spray for bugs every month? It’s nice but I could get by doing it myself. That being said it makes my life a lot easier especially if I want to travel for extended periods of time in the future. For the cost I think I get a lot of value in return. Especially the landscaper! $50/ month is a steal!!

Transportation $0 (0%)

Because I’m blind I don’t drive and it is one of my largest costs savings categories. Also since I’m retired I don’t have to pay anything to get to and from work. I live near family for special errands and can walk most places I need to. One of the great things about the internet is I can have just about anything I need delivered!

Travel $500 (9.1%)

One of my goals in life is to see as much of the world as I can before I go completely blind. I budget around $500/ month for this every month. This month I went to Utah to visit some friends and it ran a bit over $500 but it just comes out of the travel fund. The month of May I have not Trips planned so the travel fund will grow a bit.

Food $800 (14.5%)

Groceries $400

Dining/ Delivery $400

I can hear the comments section already! YOU SPEND $800 on FOOD for one person?! And to that I say YEP. I’m already retired, I don’t need to pinch every penny and going out to eat with family and friends is important to me and gets me out of the house. If I need to save some money this is a category I could easily trim.

Other $500 (9.4 %)

This last category is a mixed bag it includes everything from the vet to materials for projects around the house or occasional expenses such as a new phone or laptop to be upgraded. In the past 3 months here are some examples of what I spent in this category

Vet $661 (all vaccines and a full year of doggie meds)

Home Depot $455 (Furnace filters, new lights, propane, sand, smart thermostat etc)

Amazon $384 (soap, detergent, fish food, knife, trash bags, supplements etc)

Subscriptions: $51.95 (0.9%)

Apple Music $9.99

Netflix $9.99

*Discovery + $6.99

HBO Max $9.99

Zwift $14.99 (Exercise Bike App)

I saved subscriptions for last because it’s my smallest category but it’s a category that can get out of hand if it isn’t monitored. That’s why I keep tabs on it. I put an asterix on Discovery + since I just cancelled that swapped in Netflix (I rotate service about every 6 months to keep things fresh).

Investments:

As you know from my monthly update reports my stated goal is to save $20K per year, which works out to an average of $1,666.67 per month.

Total/ Summary

So drum roll… The total is

$6,530.62 per month or around $78,367.44 ($58,367.44 without investments)

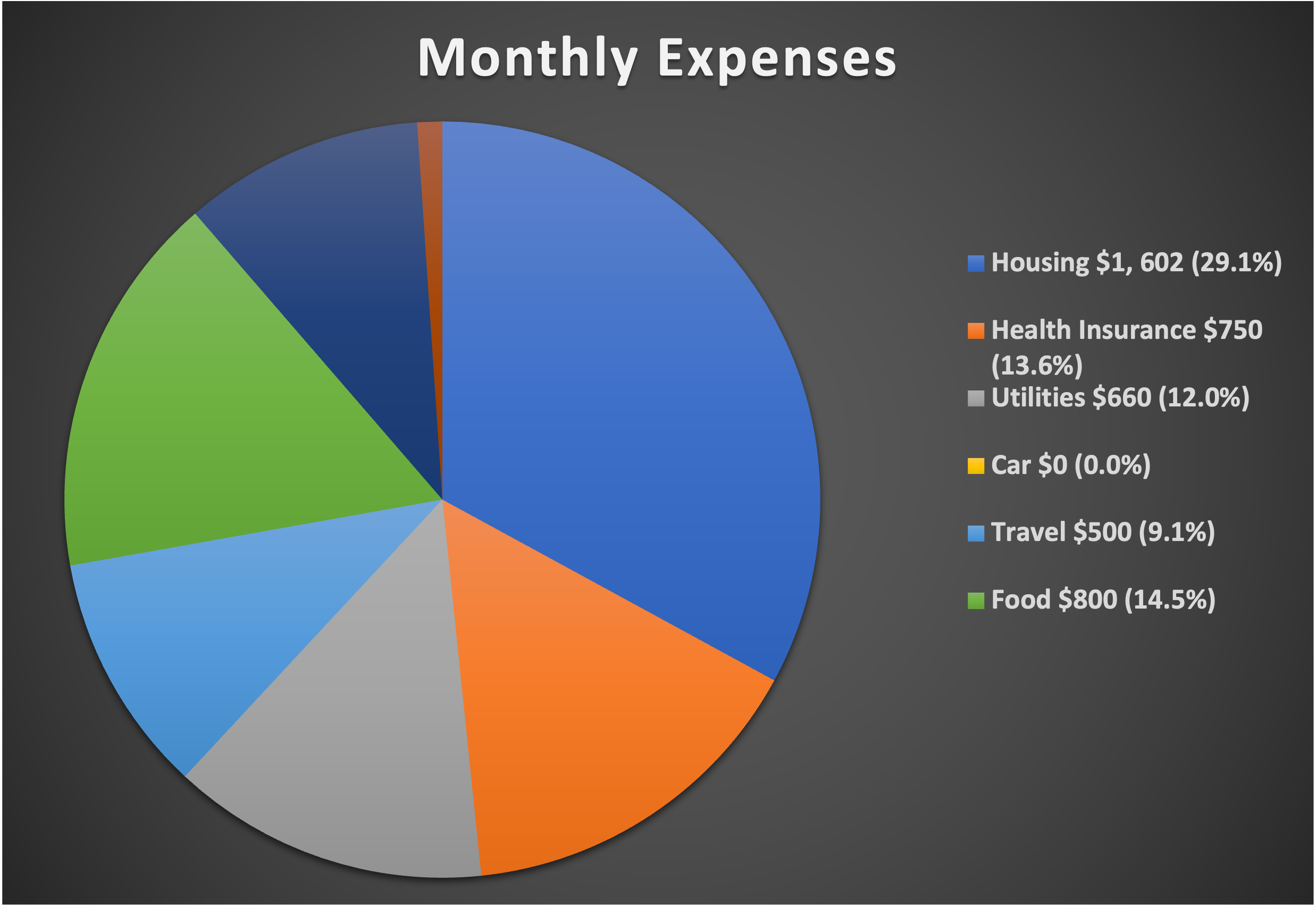

Here is a quick breakdown along with a pretty pie chart I made for you more visual folks

Funny how a chart makes it look like everything has a purpose

Who Knew being retired would be so expensive?! A couple things to keep in mind when retiring early.

You’ll likely have a house payment (Mortgage = $14,436 per year)

Medical insurance is a huge cost! for me it’s $9K per year!

Not owning a car is an enormous savings for me

As a young energetic person you’ll want to get out and do things with your free time! I don’t want to just “survive” I want to live the best life possible!

Now you sharp math folks out there will notice I said I bring in around $5,500 per month so where does the rest of the $1,030.62 per month come from? Well this is where my non passive income comes in.

Side hustle brings in on average $500 – $1,000 per month

Selling stuff on ebay $250- $400 / month

Credit Card Rewards $50 / month

Random Money $100/ month (things like escrow balance, rebates, closing old accounts etc)

It looks a little different every month but I normally have around $1,000 to $1,200 coming in from various sorces.

What am I doing to save money moving forward?

Health insurance:

The health insurance is an obvious target here. I should’ve done something sooner but with a pandemic and such going on I decided to keep my fancypants high end policy for and extra 2 years. Well I’m done with it! I’m extremely healthy with no medications or other chronic conditions so I’m shopping around for basic insurance. So far it looks like I’ve found a plan for $175/ month. It’s not very good, basically covers 80% after a $25 copay (no cap on out of pocket) but seeing as I haven’t been to a doctor for anything other than a check up in 15 years I think the $575/ month $6,900 / year savings is a no brainer. After 2-3 years I’ll have a fat savings to fall back on for any unexpected medical emergencies. Also if I develop chronic condition I can just increase my medical coverage in the November enrollment period as needed.

Property Tax:

A less obvious savings is my property Tax, in AZ a blind person can qualify for property tax exemption. Since most of my income isn’t countable (complicated not going to get into the details in this post) I quality for property tax exemption. This is a savings of $259/ month or $3,108 / year.

So with 2 changes I’ll be saving $10,096 per year! That’s double my travel budget!!

What about an emergency or economic recession?

I bring this topic up because I find people are terrified of what they can’t control, they play the what if game in their heads and can’t imagine what they would do if they quit their jobs and gasp something doesn’t go as planned. Well I’ll share what my emergency plans are as someone who’s been retired for almost 3 years. Sometimes the best thing you can do is plan on things not going according to plan.

Most of my income is passive so I’m relatively insolated from an economic recession. That being said emergencies and unexpected expenses do happen. If I something came up I have several things I can do

Cut back on expenses, discretionary spending such as travel, dining out, purchases of electronics can easily be post phoned to quickly free up free cash flow.

Reduce how much I invest. You notice from my monthly updates I don’t always invest the same amount every month. Some months I invest a large amount while other months I might have some expenses so I don’t invest as much. As long as I hit my goal of $20K per year I don’t beat myself up too much.

Put the bill on a credit card, a credit card offers 30-60 days of interest free lending depending on where you are in your payment cycle. This gives you time to come up with additional funds. I have around $80K in available credit at any point in time

Put it on a payment plan, while I’d hate to do this you can normally put things like a new roof, car, large medical expense on a payment plan to spread the costs out

I do have an emergency fund of around $5K and another $15K in IBonds for a total of $20K.

These are the easy things to do I’m sure your imagination can come up with more extreme examples that I haven’t planned for, we’ll just have to cross that bridge if and when that day comes. The fact is when you retire at age 32 you still have most of your life ahead of you and a lot can happen, it’s a risk you have to be willing to take if you want to live free of a 9-5 job. It also means you’ll need to stay flexible as your life changes you’ll likely need to make adjustments. At the end of the day I’m much more financially sound than most Americans and sleep just fine at night.

For the record the largest emergency I’ve had to date since I retired was a sudden $6,000 bill I had to pay that day. I just put it on the credit card, pulled about $3K from cash reserves and rebuilt the cash reserve over the next few months.

Conclusion

So there you have it the under the hood workings of my budget. I could certainly live more frugally than I do but I’m comfortable with my level of spending. I’m still able to save $20K per year for when my passive income sources eventually come to an end.

Make sure you Join our Community so you don’t miss out on future updates!